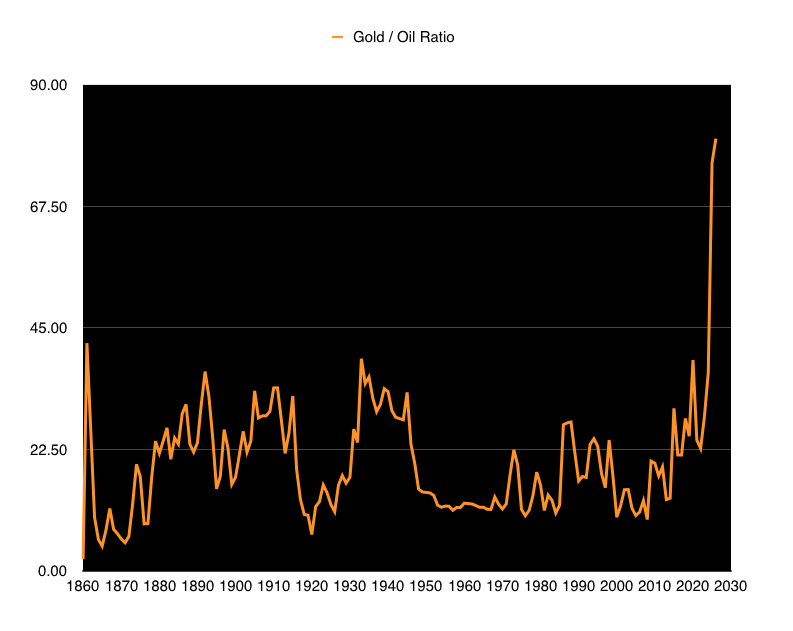

gold/oil ratio:

166 year picture of Gold/Oil Ratio:

The chart below is of the Gold/Oil Ratio - simply it is the number of barrels of oil it takes to buy one ounce of gold. Just like all market peaks - they can be massive on the upside and can quickly turn down. It is important to note that bottoms are longer in forming and can last decades. As of February 2026 this ratio now stands at 80:1. An ALL-TIME High! Our Gold target of $5,300 an oz. was achieved. A reversion to the mean presents ~ $120 a barrel of oil could be possible within the coming years. Stay tuned!

Chart updated February 2026

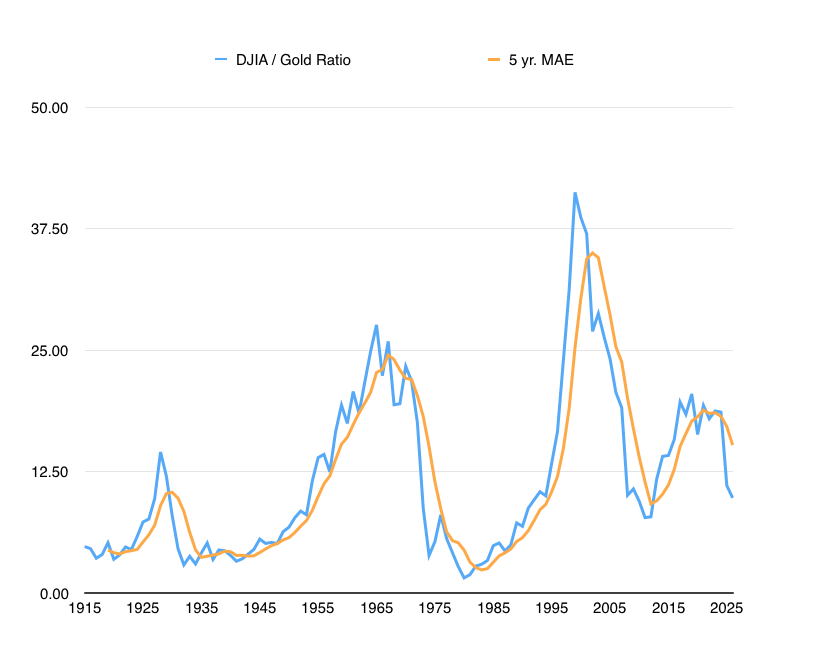

DJIA/gold ratio:

The chart below is of the Dow/ Gold Ratio. The rising blue line indicates the Dow is outperforming Gold - this happens during structural bull markets in equities. When the line is declining, Gold shows an outperformance vs. the Dow (during equity bear markets). Peaks in the stock market during 1929, 1966, and 2000 gave way to structural changes in the market for equites. A modest reversion to the norm where the ratio of 7:1 can be seen - would equate to Gold ~ $6,000 - $12,000. Currently we are at ~10:1 ratio. Stay tuned.

Chart updated as of February 2026

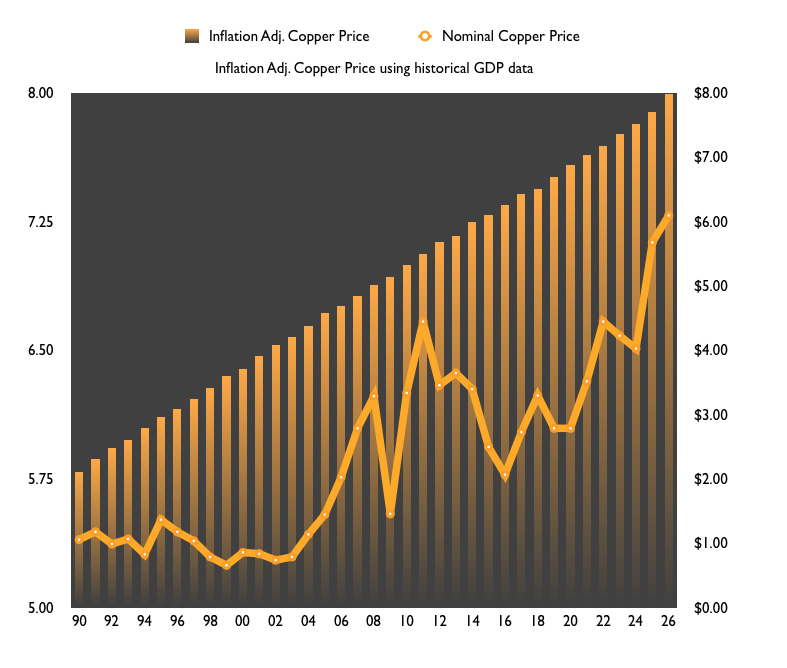

inflation adjusted copper:

Long-Term Inflation Adjusted levels for Copper indicate a price of ~ $8.00 lb. Current ratio of Copper/Gold presents a rational indication of Copper at ~ $11 lb. A lack of discoveries, on top of 20 year build-out for new mines, could prove bullish for copper.

Chart updated February 2026

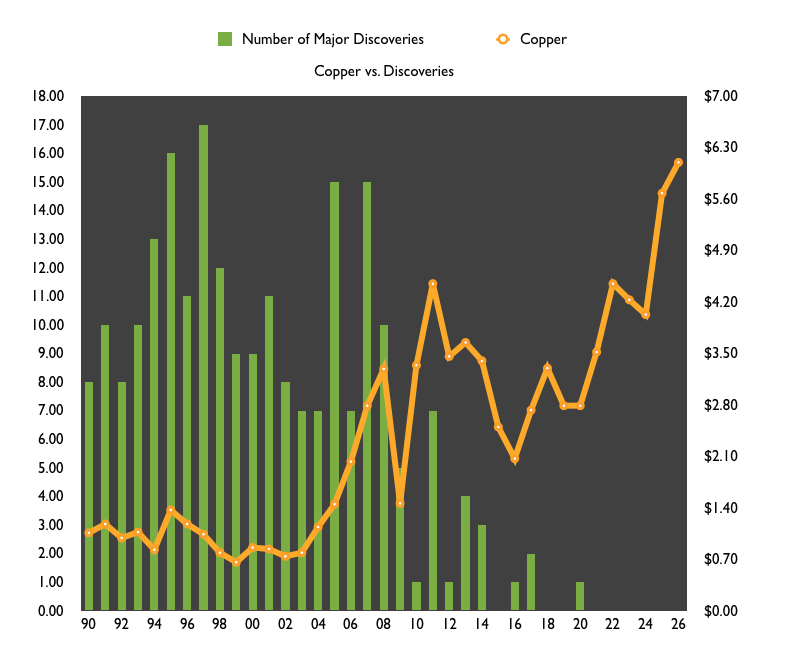

copper Vs. discoveries:

Chart updated February 2026

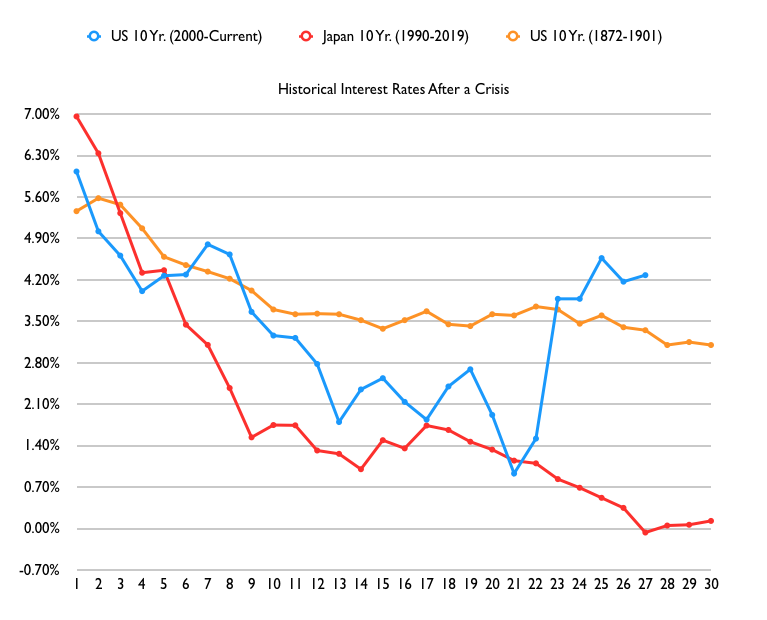

historical interest rates after a crisis:

A bottoming formation in the US 10 yr. Government Bond is following prior patterns seen both in the U.S. and Japan following past crises. Two Hundred and Fifty years of interest rate data confirms this theory, as bottoms usually take years to form versus tops that are sharp in nature when they peak. Current Taylor Rule indicates that rates should be 2.90%.

Chart updated as of February 2026

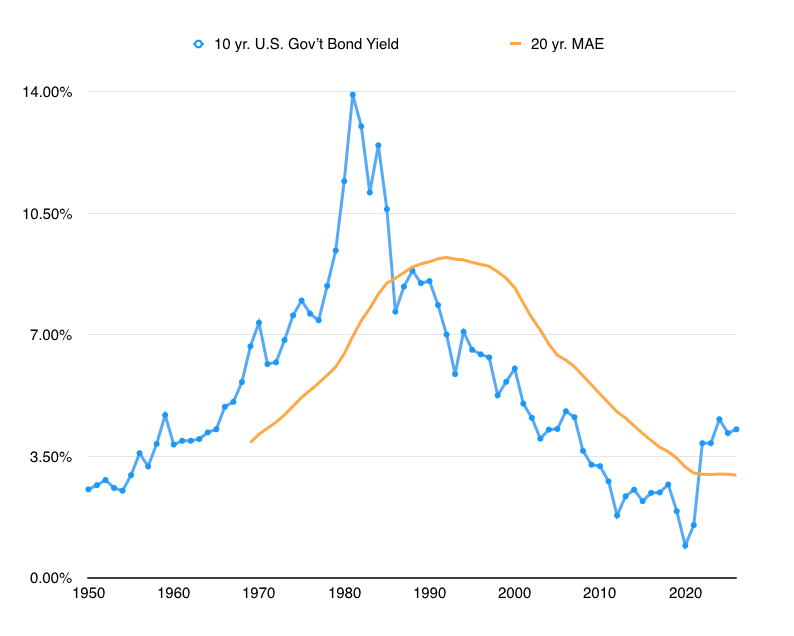

10 yr. U.S. Government yield chart:

The chart below hit a high of 13.92% in 1981 and a low of .93% in 2020 on a yearly basis. The overall picture appears that interest rates have consolidated. 10 and 20 year Moving Averages HAVE CROSSED! This would indicate that we could witness a major reversal in interest rates. Stay tuned.

Chart updated as of March 2026

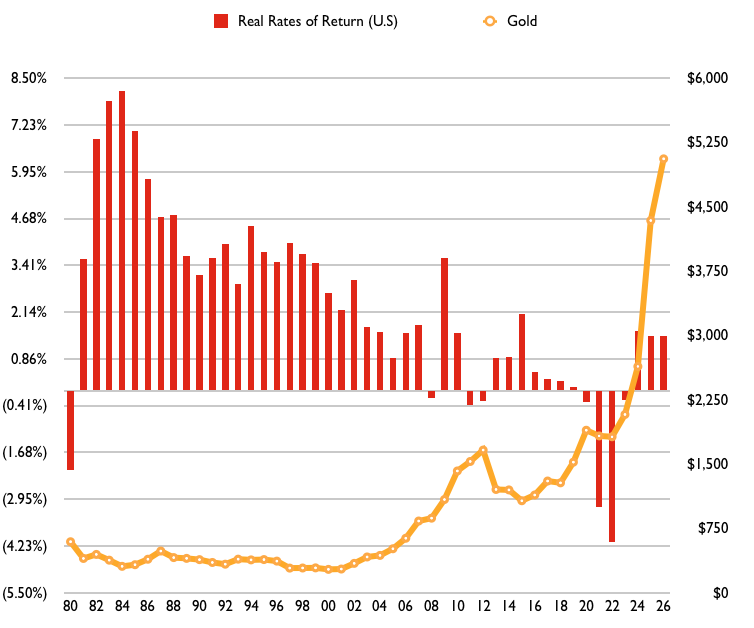

Real Rates of Return:

Long term Real Rates of Return (10yr. Treasury Bond - Inflation) have been generally declining for 40 years. Currently the United States Real Rate of Return is 1.29%. Globally that number is 1.12%.

Chart updated as of February 2026

inflation data:

Long-Term Inflation data dating back from 1774

Two Hundred and Fifty-Two years of data show that historic inflation averages 1.80%. 30 year cycles appear present. This would indicate that the bottom of our declining rate of inflation to happen around 2023. Just two years ago, Congressional Budget Office estimates were for estimated inflation trends to cross by 2025 - implying a structural change in trend. This has now happened and indicates a 10-15 year cycle of rising inflation. Watch what Congress has budgeted - this helps weed through the noise.

Chart updated as of March 2025

Margin Debt: All-time high

Since 1961 Margin Debt has increased at an annual rate of 9.21% while the S&P 500 in that same time frame has offered an average return of 7.12% not including dividends. U.S. Treasuries offered an average return of 5.82% while Inflation was 3.78%.

Chart updated as of March 2025

Global oil markets chart:

Supply vs. Demand

The chart below shows data from the International Energy Agency (IEA) and the U.S. Energy Information Administration (EIA). Putting things into perspective - there really was not an oversupply in the global oil markets. Given the latest developments this year, global supply / demand is on par with each other. By decade end, more production will need to come on line in order to prevent an imbalance. Back in 2019, the IEA had estimated massive shortfalls in global supply. They simply got it wrong. That being said, extensive investment in existing fields needs to continue for supply and demand to stay in check. This could produce a risk to price spikes for oil. Stay tuned!

Chart updated as of March 2025

Buffett Indicator:

This chart is one of the best indicators of where valuations in the equity market present themselves. Central Bank money printing is having a dramatic cause and effect relationship with all global asset classes.

“Shaw Group expects another $1 trillion will be printed in the next 3-5 years”. Back in March of 2020 when we penned this - little did we think this $1 trillion would come on so fast. This added $1 trillion would have placed in a potential rally of another 17% to equities and 4% to all assets. Thus placing in a target ratio of 1.7165%. TARGET HIT!

Current data shows this ratio to now stand at 2.05%. ~2.30% would indicate a level of overvaluation comparable to 2000. Stay careful.

Chart updated as of March 2025

The World bank gdp annual growth data:

Chart updated October 2024

U.S. Leverage View:

Chart updated as of October 2024

COrporate Profits/S&P 500

Corporate Profits After Tax vs. S&P 500

U.S. ISM Purchasing Managers Index

ISM purchasing managers index: 40 year

The ISM Index surveys non-manufacturing (or services) firms' purchasing and supply. The services report measures business activity for the overall economy; above 50 indicating growth, while below 50 indicating contraction. As of 11/2023, the current reading is 46.7 representing a possible basing in the U.S. Economy?

Chart updated January 2024

oil production: yearly

G-SIB's (Global Systemically Important Banks):

A negative year for 2022. $19 trillion in assets need to be sold compared with approximately $1.550 trillion in equity that needs to be added to the list of 30 G-SIBI’s. This is a sharp rise from 2021 - a 15% increase or ~ $200 billion from a year ago. The United States, France and Japan will need to make the most headway in adding capital to their banks in the years to come. All Central Banks printing of money has amounted to a zero sum over the last 11 years.

Basel III G-SIB's need for capital

Capital needed per country: Banking/Finance sectors

The United States, France, Japan, and England have the most to consider in how they raise capital for the banking sectors in relation to their economic footprint. Expect to see equity to increase on company balance sheets during 2023-2027.

Chart updated as of Dec. 2022

S&P 500 index p/e ratio chart:

This chart shows historical P/E Ratios for the S&P 500. Over the last 20 years the S&P 500 has tended to bottom at a rolling P/E Ratio of 15. This offers a clear picture of where valuations stand today.

Chart updated as of July 2021

The views expressed here represent the opinion of Shaw Group, LLC. and are not intended to predict or depict performance of any investment. Material discussed herein is meant for general illustration and/or informational purposes only and should not be used or construed as investment advice or an offer to buy or any endorsement, recommendation or sponsorship of any company or security by Shaw Group, LLC. Although the information has been gathered from sources believed to be reliable, please note that individual situations can vary. Shaw Group, LLC. does not guarantee the suitability or potential value of any particular investment or information source. Therefore, the information should be relied upon only when coordinated with individual professional advice. With any investment vehicle, past performance is not a guarantee of future results. No information should be interpreted to state or imply that past results are an indication of future performance. Investors should be aware that there are risks inherent in all investments such as fluctuations in and potential loss of investment principal. Investors need to be aware that no investment plan or asset allocation can completely eliminate the risk of fluctuating prices and uncertain returns. You acknowledge that any requests for information are unsolicited and shall neither constitute nor be construed as investment advice by Shaw Group, LLC. to you. Shaw Group, LLC. may invest or otherwise hold an interest in companies or securities discussed on shawadvisors.com.

Contact us!

We share our insight regarding global capital markets and investment themes via proprietary analysis.